Choosing the Right Medicare Plan for You

Choosing Medicare coverage can feel overwhelming. There are many options, each with its own benefits, costs, and rules. But with the right information, you can make a confident choice that fits your health needs and budget. I’m here to walk you through the process step-by-step, so you feel empowered and clear about your Medicare options.

Understanding Your Medicare Coverage Options

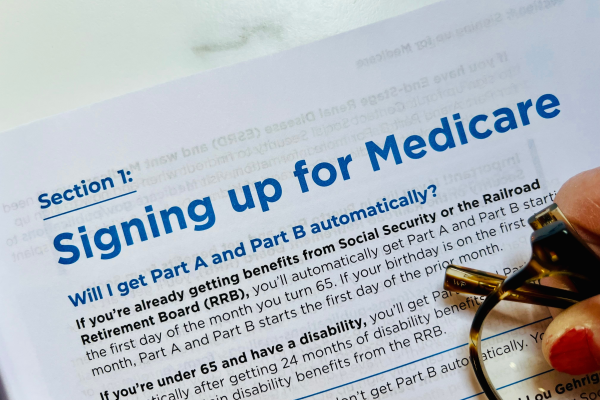

Medicare is a federal health insurance program primarily for people 65 and older, but also for some younger individuals with disabilities. It has several parts, and knowing what each covers is the first step in choosing the right plan.

- Part A (Hospital Insurance): Covers inpatient hospital stays, skilled nursing facility care, hospice, and some home health care.

- Part B (Medical Insurance): Covers doctor visits, outpatient care, preventive services, and some home health care.

- Part C (Medicare Advantage): An alternative to Original Medicare (Parts A and B) offered by private companies. These plans often include extra benefits like vision, dental, and prescription drugs.

- Part D (Prescription Drug Coverage): Helps cover the cost of prescription medications.

When you start exploring plans, think about your current health needs and what you expect in the future. For example, if you take several medications, a plan with strong drug coverage is important. If you want extra benefits like dental or vision, a Medicare Advantage plan might be a better fit.

Medicare brochures help explain different coverage options clearly.

Tips for Choosing Medicare Coverage That Fits Your Needs

Choosing Medicare coverage means balancing your health needs, budget, and preferences. Here are some practical tips to guide you:

- Review Your Current Health Care Usage: Look at your doctor visits, hospital stays, and prescriptions from the past year. This helps you estimate what coverage you need.

- Compare Costs Carefully: Don’t just look at monthly premiums. Consider deductibles, copayments, coinsurance, and out-of-pocket limits.

- Check Provider Networks: If you have preferred doctors or hospitals, make sure they accept the plan you choose.

- Look for Extra Benefits: Some Medicare Advantage plans offer perks like gym memberships, transportation to medical appointments, or wellness programs.

- Use Online Tools: The Medicare Plan Finder tool or trusted insurance advisors can help you compare plans side-by-side.

Remember, choosing medicare plans is easier when you have clear, personalized information. Don’t hesitate to ask questions or get help from a licensed agent who understands your local options.

Using online tools can simplify comparing Medicare plans.

What are the biggest mistakes people make with Medicare?

Many people make avoidable mistakes when selecting Medicare coverage. Knowing these pitfalls can help you avoid costly errors.

- Waiting Too Long to Enroll: Missing your initial enrollment period can lead to late penalties and gaps in coverage.

- Choosing Based on Premium Alone: A low monthly premium might mean higher out-of-pocket costs later.

- Ignoring Prescription Drug Coverage: Not enrolling in Part D or a plan with drug coverage can lead to high medication costs.

- Not Reviewing Plans Annually: Medicare plans change every year. What worked last year might not be the best choice now.

- Overlooking Network Restrictions: Some Medicare Advantage plans have limited provider networks, which can restrict your access to preferred doctors.

By being aware of these mistakes, you can take steps to avoid them. For example, mark your calendar for enrollment periods and review your plan every fall during the Annual Election Period.

Marking important Medicare enrollment dates helps avoid penalties.

How to Enroll and When to Make Changes

Knowing when and how to enroll in Medicare is just as important as choosing the right plan.

- Initial Enrollment Period: This is a 7-month window around your 65th birthday (3 months before, the month of, and 3 months after) to sign up for Parts A and B.

- General Enrollment Period: If you miss your initial window, you can enroll between January 1 and March 31 each year, but coverage starts July 1.

- Annual Election Period: From October 15 to December 7, you can switch Medicare Advantage plans, change from Original Medicare to Medicare Advantage, or join/leave a Part D plan.

- Special Enrollment Periods: Certain life events like moving or losing other coverage allow you to make changes outside the usual windows.

When enrolling, gather your personal information, Social Security number, and details about your current health coverage.

Making Medicare Work for You Every Year

Medicare isn’t a “set it and forget it” program. Your health needs and plan options can change, so it’s important to review your coverage annually.

- Check for Plan Changes: Premiums, copays, and covered drugs can change each year.

- Assess Your Health Needs: New medications or health conditions might mean a different plan suits you better.

- Use the Annual Election Period: This is your chance to switch plans if needed.

Staying proactive helps you avoid surprises and ensures your coverage matches your needs.